Two foreigners sit in the same Davao café. Both invoice overseas clients, both hold money in foreign accounts, both love the mango shakes. One of them owes the Philippines nothing on his worldwide income and holds a tax residency certificate his home bank accepts without blinking. The other just discovered that a single local contract he signed is being taxed at 25% of gross — no deductions, no expenses, no appeal to fairness.

The difference between them isn't income, nationality or luck. It's classification. Philippine tax law sorts foreigners into categories, and everything — your rate, your base, your paperwork, your standing with banks — flows from which box you're in. This page explains the boxes, how to get into the right one, and what it looks like in practice.

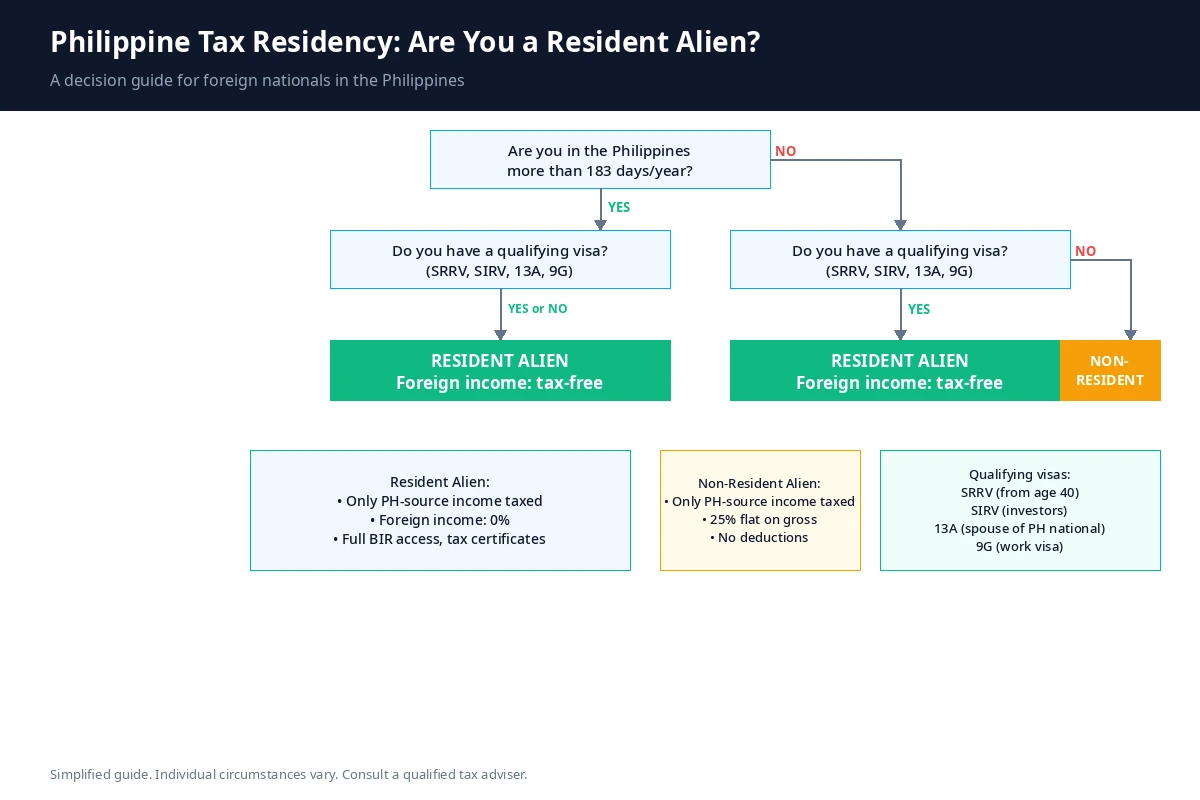

The three classifications

1. Resident Alien — the status to aim for. You qualify by either of two routes: physical presence of more than 183 days in a calendar year, or holding a visa indicating permanent or long-term residence — the SRRV, SIRV, 13A or 9G. The second route is the one most guides miss: with the right visa, you're a resident alien *without counting days*, which is exactly what internationally mobile people need.

What it gets you: taxation only on Philippine-source income, at progressive rates (topping out at 35%) on a net basis with deductions; full registration with the Bureau of Internal Revenue — your own TIN, proper returns, and on request a Certificate of Tax Residency for your home-country tax office or bank. Foreign-source income — dividends, capital gains, rents, salaries, crypto realized abroad — sits entirely outside the Philippine net, even when remitted into the country.

2. Non-Resident Alien Engaged in Trade or Business (NRA-ETB). No residency, but economic activity in the Philippines and presence beyond 180 days in aggregate. Philippine-source income is taxed at the same progressive rates — but without the resident's full system access, and with a status that raises more questions than it answers at banks.

3. Non-Resident Alien Not Engaged in Trade or Business (NRA-NETB). The expensive box. Short-stayers with no sustained activity pay a flat 25% on gross Philippine-source income. Gross means gross: no expenses, no allowances, nothing. The classic way in: a traveler picks up one local engagement and meets Philippine withholding at full strength.

Why resident alien status is worth engineering

Put the three side by side and the strategy writes itself. The resident alien is the only category that combines the territorial exemption on foreign income, net-basis progressive taxation on anything local, and full standing in the BIR system. That last part matters more than it sounds: the TIN and registration are prerequisites for a bank account, the ACR card and most official processes — and the Certificate of Tax Residency is the document that turns "I moved abroad" from a claim into evidence when your home tax authority or your brokerage asks.

Our standing recommendation to every client who intends to live here: position yourself deliberately as a resident alien — through presence if your life is here anyway, or through visa status if you want the classification without the day-counting. This is not aggressive planning; it's choosing the door the law explicitly built for you.

The practical build: TIN, BIR registration, nil returns

Becoming a resident alien on paper is a sequence, not an event, and the order matters because each step gatekeeps the next:

- 1

A real address

A residential lease in your name. Every registration downstream references it.

- 2

TIN

Your Philippine tax identification number, issued by the BIR. Required for banking and nearly everything official.

- 3

BIR registration as a resident alien

Your formal entry into the system. Note the distinction we insist on with every client: this registration confirms you are *registered for tax* in the Philippines; the Certificate of Tax Residency is a separate document obtained afterwards through its own process. Banks generally need the first at setup; home-country authorities eventually want the second.

- 4

Annual filing

Required if you have Philippine-source income. If you don't, many clients file a voluntary nil return: zero income declared, registration kept demonstrably alive, and the path to the residency certificate kept friction-free. Minutes of paperwork buying years of clean documentation.

This is the core of what we build for clients — most of it remotely, with the on-site steps compressed into a short Davao visit.

A worked contrast: the same income, three classifications

Take a consultant earning $60,000 from overseas clients who also picks up one $10,000 Philippine engagement during the year:

- •As a resident alien: the $60,000 foreign-source income is entirely outside the Philippine net. The $10,000 local engagement is taxed at progressive rates on a *net* basis — expenses deducted, allowances applied — typically leaving a modest liability, cleanly filed on a proper return with a TIN behind it.

- •As NRA-ETB: same $10,000 taxed at the progressive rates, but with a weaker standing in the system and a classification that makes every bank conversation harder.

- •As NRA-NETB: the $10,000 meets a flat $2,500 withholding — 25% of gross, expenses irrelevant, plus the foreign income now sits behind a status that documents nothing about where this person actually lives.

Same person, same money, three very different outcomes — decided entirely by classification. The $60,000 was never at risk in any scenario; the point is what happens to everything that touches the Philippines, and what paperwork exists when anyone asks where you're tax-resident.

Keeping the status: what breaks it

Residency is a state, not a trophy — it persists as long as its basis does. The visa route is the durable one: an SRRV or 13A holder remains a resident alien through travel-heavy years without day-counting. The presence route needs the days each year it's relied on. What actually breaks things in practice is rarely the law and usually the paper: a lapsed visa nobody renewed, a lease that quietly ended, a registration left dormant so long the certificate process stalls. The maintenance routine — visa renewals on calendar, lease continuity, the annual nil return — is unglamorous and takes hours per year. It's also the difference between a residency that performs under scrutiny and one that dissolves at the first serious question.

What residency here does *not* do

Honesty section, because the internet oversells this:

- •It doesn't end your home-country obligations by itself. Americans keep filing with the IRS regardless — the treaty page covers that machinery. Europeans need a clean exit from their home tax net before Philippine residency means what they want it to mean.

- •It doesn't make Philippine-source income tax-free. Take a local job, rent out a Davao condo, trade on the local exchange — that's all taxable here at normal rates. The exemption is about *foreign* source, and the source lines deserve deliberate mapping.

- •It doesn't survive sloppiness. A residency built on nothing — no lease, no TIN, no presence pattern, no registration — is a story, not a status. When a bank or foreign tax office probes, documents win and stories lose. This is the entire reason our model is a real base with real paperwork rather than a mail-forwarding address.

Common misconceptions, corrected

"I need to stay 183 days or I lose the status." No — the visa route exists precisely so you don't. An SRRV holder with heavy travel remains a resident alien.

"Money I bring into the country becomes taxable." No — taxation follows the *source* of income, not the movement of money. Remitting foreign earnings to a Philippine account changes nothing.

"Tourist status means the Philippines can't tax me." Wrong twice: tourists can become tax residents through presence alone (past 183 days), and tourists who earn Philippine-source income get the NRA treatment — potentially the 25% gross rate. Visa status and tax status are related but separate tracks.

"The registration and the residency certificate are the same thing." They're not, and conflating them is the most common documentation error we untangle. Registration first, certificate after — each has its own use case.

Frequently Asked Questions

How does the Philippines decide if I'm a tax resident?

Two independent routes: more than 183 days of physical presence in a calendar year, or holding a long-term visa such as the SRRV, SIRV, 13A or 9G. Either one suffices.

Do resident aliens pay Philippine tax on foreign income?

No. Resident aliens are taxed only on Philippine-source income. Foreign dividends, capital gains, rents, salaries and crypto realized abroad are outside the net — even when remitted.

What's the tax rate if I'm not a resident?

Philippine-source income of non-residents engaged in business is taxed at the normal progressive rates; non-residents *not* engaged in business pay a flat 25% on gross, with no deductions.

Can I get a certificate proving my Philippine tax residency?

Yes — the Certificate of Tax Residency from the BIR, obtainable after proper registration. It's the standard evidence for home-country tax offices and banks.

Do I have to file a return if I have no Philippine income?

Not necessarily — but a voluntary nil return keeps your registration demonstrably active and smooths the path to the residency certificate. We file them for most clients as routine.

Does a tourist visa block tax residency?

No. Presence past 183 days can make even a tourist a resident for tax purposes. Visa status and tax status are separate questions — which cuts both ways, and is worth using deliberately rather than discovering accidentally.